Зерттеу

23.05.2026,

в 12:00

2513

This story involving Tethys Petroleum has it all: offshore structures, family ties, state funds, advance payments for nothing, and sudden financial miracles. But there is also a point where the miracles come to an end. That point is January 2022.

In the summer of 2018, Tethys Petroleum, operating in the Aktobe region, announced the arrival of new investors — not global corporations, but companies with little-known names: Jaka Partners FZC and Gemini IT Consultants DMCC. The deal was valued at just $1.2 million, but the key point was not the amount, it was the names involved.

Jaka Partners FZC is headed by Kalamkas Turman, the wife of Ibulla Serdiev, who at the time was chairman of the national company QazaqGaz. Gemini IT Consultants DMCC is controlled by Korlan Sharipbaeva, the daughter of Kairat Sharipbaev, then chairman of the board of KazTransGas and later chairman of QazaqGaz. Kazakh media have also described him as the second husband of Dariga Nazarbayeva, the eldest daughter of Kazakhstan’s first president.

Through APL Construction LLP, where Korlan Sharipbaeva is also the ultimate beneficiary, family-linked structures hold an additional 4% stake. In total, 27.58% of Tethys Petroleum’s shares ended up in the hands of relatives of senior executives at the state-owned company purchasing gas from Tethys.

A coincidence? The subsequent course of events suggests otherwise.

Until September 2018, the national gas operator purchased gas from Tethys at 44.18 dollars per thousand cubic meters. Immediately after the entry of the new shareholders, the price nearly tripled, rising to 122.48 dollars per thousand cubic meters.

The company’s report for the first quarter of 2019 states: “Gas was sold at a net average price equivalent to $122.48 per Mcm… compared with $44.18 in Q1 2018.”

Not a typo. Not a market spike. Not force majeure. A private company, in which nearly a quarter of the shares were held by relatives of QazaqGaz’s leadership, suddenly began receiving a price three times higher than before.

Other producers, like dutiful workers on the gas front, continued supplying raw materials to the national grid at tariffs approved by the Ministry of Energy. Meanwhile, Tethys operated at a price that, within the industry, was referred to as nothing other than a «family tariff».

A 2024 analytical review of the gas industry states: «Gas purchase prices from subsoil users have consistently been below the cost of production». In other words, the state purchased gas from producers at suppressed prices in order to keep tariffs low for the population.

This fact strongly suggests that the purchase of gas from Tethys at 122.48 dollars per thousand cubic meters was a rare exception rather than standard market practice. Apparently, for some, the definition of «the population» had been narrowed to a circle of shareholders.

In 2023, QazaqGaz began partial liberalization, introducing a new gas purchase pricing formula: «Price = production cost + processing + transportation + 10% profitability».

However, even under this formula, experts estimate that the price could not have exceeded 70 dollars per thousand cubic meters.

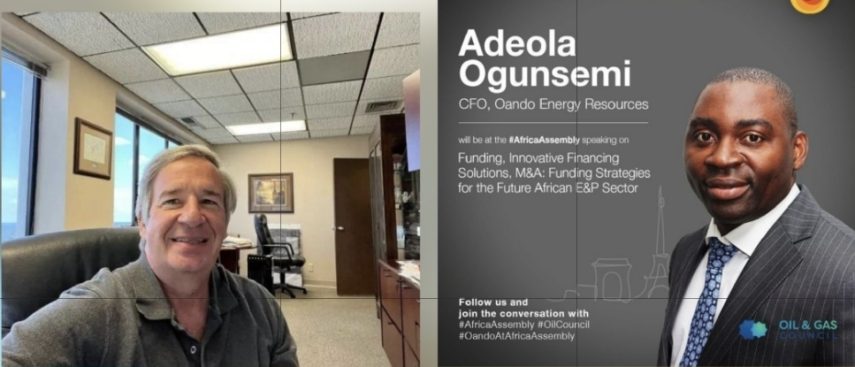

Thus, the arrival of the new shareholders became the most profitable development for the top management of Tethys Petroleum. And it is worth naming them explicitly: first and foremost, William P. Wells, Chairman of the Company’s Board of Directors. And here are his colleagues, who are tasked with ensuring that the company conducts its business transparently and in full compliance with the laws of both Kazakhstan and Canada, where its shares are listed: Adeola Ogunsemi, independent director (Chair of the Audit Committee); Mattias Sjoborg, independent director (Chair of the Remuneration and Nomination Committee); and Don Streu, independent director — who, notably, is also the Honorary Consul of the Republic of Kazakhstan in the province of Alberta and a member of the National Council of the Canada-Eurasia Chamber of Commerce (CECC).

According to the 1963 Vienna Convention on Consular Relations, one of the principal functions of an honorary consul is to facilitate business contacts between countries, support trade missions, and promote humanitarian and cultural ties. At the same time, the Convention explicitly prohibits the use of such status to advance private interests or obtain commercial benefit, especially from a state-owned company in the host country.

Now to the commercial benefit, which we will attempt to calculate. The starting figures are as follows:

In plain terms, that amounts to 31.32 million dollars in excess profit.

This was not merely a favorable contract. It is a scheme in which a state-owned company pays inflated prices to a private firm whose shareholders include relatives of the very executives running that state company — relatives who directly profit through dividends.

And the cherry on top: an advance payment for gas that had not yet been produced. In April 2020, TethysAralGas received a 7.6 million dollars prepayment from QazaqGaz for gas that had not even been extracted. As stated in the company’s press release: “TethysAralGas LLP has received a prepayment of approximately US$7.6 million from its gas customer”.

It is difficult to imagine any other private producer receiving such a «gift». After obtaining more than 7 million dollars, the company partially repaid its debts, drilled new wells, and ultimately restored production and improved its financial position.

In effect, the state financed a private company whose shareholders included relatives of executives running the very same state-owned enterprise. Is this not a textbook conflict of interest?

After the January 2022 events, Kairat Sharipbaev lost his position, the Financial Monitoring Agency placed Ibulla Serdiev on an international wanted list, and the «Old Kazakhstan» lost its political influence.

Then came miracle number two: QazaqGaz stopped purchasing gas from Tethys at inflated prices.

Without political backing, Tethys Petroleum instantly lost access to its superprofits. Just yesterday, the company was awash in advance payments, now it found itself back in financial difficulty.

The story of Tethys Petroleum is a textbook case in political economy, illustrating how:

— state resources are transformed into private assets,

— a state-owned company purchases from insiders at inflated prices,

— profits are privatized,

— and losses are socialized.

While Old Kazakhstan retained control of the levers of power, the scheme worked flawlessly. Once those levers disappeared, so did the profits.

On Tuesday, we sent formal inquiries to William P. Wells, Chairman of the Board of Directors of Tethys Petroleum Ltd., and Adeola Ogunsemi, Chair of the company’s Audit Committee. We expect to receive their responses next week.

SHARE YOUR OPINION AND DISCUSS THE ARTICLE ON OUR TELEGRAM CHANNEL!

25.07.2026,

12:00

22.07.2026,

18:00

21.07.2026,

10:30

23.07.2026,

13:30

27.07.2026,

10:30